TMZ has a story this morning: "Aaron Carter died without a will... so now the State of California will decide who inherits his estate."

This is commonly found on lawyers' web sites and blog posts. "If you don't have a will, the state will decide where your property will go." That statement is untrue.

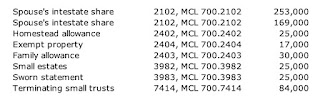

Each state has intestacy statutes, which provide a priority of inheritance if a person dies without a valid will. Those intestacy provisions apply only to "probate assets," that is, assets owned by the decedent in his own name. They do not apply to assets held in trust, to jointly-owned property, to property with transfer on death directions, or to retirement accounts (unless the owner did not make a beneficiary designation.)

What is true is that, if you do not want that order of priority followed, you need a will, a trust, or some other mechanism to make sure that does not happen.

The intestacy statute is intended and designed to follow what most people would want to happen to their money. The priority is, in general, spouse, children, parents, siblings, their children (nephews and nieces), grandparents, and their descendants (cousins).

It is emphatically not the case that a probate judge in California will make a decision about who will receive Carter's assets. The court will simply follow the intestacy laws.